What Does Medicare Actually Cover for Senior Care? The Honest Truth (2026 Guide)

Understanding Medicare coverage for senior care can mean the difference between financial security and financial disaster for your family.

After 13 years of running a home health agency in Texas and over 30 years as a registered nurse, I can tell you the single biggest financial mistake families make when planning for a loved one’s care: they assume Medicare will cover most of it.

It won’t. And by the time families realize this, they’ve already made decisions based on a plan that doesn’t exist.

This guide is the article I wish every family would read before they need care. I’m going to walk you through what Medicare actually covers, what it doesn’t, the hidden pitfalls of Medicare Advantage plans, the disappointing reality of Medicare equipment, and the one piece of advice that could save your family thousands of dollars. This comes from someone who dealt with Medicare every single day for over a decade — not from someone who read a government brochure.

Understanding the Basics — Medicare Part A vs Part B

Before we get into specifics, you need to understand how Medicare is structured. Medicare has multiple parts, and each one covers different things.

Medicare Part A is sometimes called hospital insurance. It covers inpatient hospital stays, skilled nursing facility care after a qualifying hospital stay, hospice care, and some home health services. Most people don’t pay a monthly premium for Part A because they or their spouse paid Medicare taxes while working for at least 10 years.

Medicare Part B is sometimes called medical insurance. It covers doctor visits, outpatient care, certain home health services, durable medical equipment, and preventive services. In 2026, the standard Part B premium is approximately $185 per month, and the annual deductible is $257.

Medicare Part C is Medicare Advantage — these are private insurance plans that bundle Part A and Part B together, often with additional benefits. We’ll talk about the significant pros and cons of these plans below.

Medicare Part D covers prescription drugs. It’s a separate plan you enroll in, and the costs vary widely depending on which plan you choose.

Understanding which part covers what is critical because families constantly mix them up — and that confusion leads to nasty financial surprises.

What Medicare Covers for Home Health Care

Medicare covers home health care — but only under very specific conditions. This is where most of the confusion and frustration begins.

To qualify for Medicare home health services, your loved one must meet all four of these requirements at the same time:

First, a doctor must order the care. A physician, nurse practitioner, or physician assistant must certify that your loved one needs home health services and create a written plan of care. Without this doctor’s order, Medicare will not pay for anything — period.

Second, your loved one must be homebound. This does not mean they can never leave the house. It means leaving home requires a considerable and taxing effort. They can still go to medical appointments, attend church, go to adult day care, or get a haircut. But if they need help from another person or a device like a walker or wheelchair to leave the house, or if their condition makes leaving inadvisable, they generally qualify as homebound.

Third, they must need skilled care. This means they require skilled nursing (wound care, IV therapy, medication management, catheter care, injections, disease education) or skilled therapy (physical therapy, occupational therapy, or speech therapy). Simply needing help with bathing, dressing, or meals is not enough on its own — there must be a skilled need.

Fourth, the care must be part-time or intermittent. Medicare typically covers up to 8 hours per day of combined skilled nursing and aide services, with a maximum of 28 hours per week. In some situations, this can be extended to 35 hours per week for a short period. Medicare does not cover 24-hour care, live-in caregivers, or long-term continuous care at home.

If your loved one meets all four criteria, Medicare covers these services at no cost to the family — no copay, no deductible for home health services:

Skilled nursing visits for wound care, medication management, IV therapy, injections, catheter care, patient and caregiver education, and disease management.

Physical therapy to improve strength, mobility, and balance — or to maintain current function and prevent decline.

Occupational therapy to help with daily activities and improve independence.

Speech-language pathology for speech, language, and swallowing difficulties.

Medical social work services to help with emotional, social, and financial concerns related to the illness.

Home health aide services for personal care like bathing, dressing, and grooming — but only if skilled nursing or therapy services are also being provided. The aide cannot be the only service.

Certain medical supplies related to the plan of care, like wound dressings and catheters.

What Medicare Does NOT Cover at Home

This is the list that catches families off guard:

24-hour home care or live-in caregivers. Medicare is not a long-term care program. It is designed for short-term, skilled, intermittent care to help someone recover or stabilize — not for ongoing custodial support.

Homemaker services on their own. Cooking, cleaning, laundry, and grocery shopping are not covered unless a home health aide provides them as part of a broader plan that includes skilled services.

Personal care alone. If your loved one only needs help with bathing and dressing but has no skilled nursing or therapy need, Medicare will not pay. This is the most common reason families are denied coverage, and it’s the one that causes the most frustration.

Meal delivery services. Programs like Meals on Wheels are wonderful, but they are not covered by Medicare.

Companionship. If your parent is lonely and needs someone to sit with them or take them for walks, that is not a Medicare-covered service.

Prescription medications at home. Part D covers prescriptions separately — home health coverage under Part A and B does not include drug coverage.

How Long Does Medicare Home Health Last?

There is no fixed day limit for Medicare home health. Coverage continues as long as your loved one continues to meet all four eligibility criteria and the doctor recertifies the need every 60 days.

I’ve had patients receive Medicare home health services for months — sometimes over a year — as long as there was a documented skilled need and they remained homebound. However, Medicare will stop coverage when the skilled need has been fully met, the patient is no longer homebound, or the doctor discontinues the order.

An important protection families should know about: the Jimmo settlement established that Medicare cannot deny home health coverage simply because a patient is not improving. If skilled care is needed to maintain current function or slow a decline, that is a valid reason for continued coverage. You do not have to show progress to keep your benefits.

What Medicare Covers in a Skilled Nursing Facility

If your loved one needs care in a skilled nursing facility after a hospital stay, Medicare Part A may cover it — but the rules are strict and the coverage is limited.

To qualify, your loved one must have had a qualifying inpatient hospital stay of at least 3 consecutive days. Time spent in the emergency room or under observation status does not count toward those 3 days — and this is a trap that catches many families. If the hospital classified your loved one as “observation” rather than “inpatient,” they may not qualify for SNF coverage even after being in the hospital for several days.

If they qualify, here’s what Medicare covers:

Days 1 through 20: Medicare pays 100% of covered services. No cost to the family.

Days 21 through 100: The family pays a daily coinsurance of $217 per day in 2026. Medicare covers the rest. If you have a Medigap supplemental policy, it may cover this coinsurance.

Days 101 and beyond: Medicare pays nothing. The family is responsible for 100% of the cost. At current Texas rates, that can be $7,000 to $7,500 per month for a private room.

Coverage also ends if your loved one’s care shifts from “skilled” to “custodial” — meaning they no longer need active medical treatment or therapy and are simply receiving help with daily activities. This transition can happen quickly, and families are often surprised when coverage stops well before day 100.

Medicare and Assisted Living — The Hard Truth

Here’s the blunt truth: Medicare does not pay for assisted living. Not the room, not the board, not the monthly rent. Assisted living is not considered a medical facility under Medicare — it’s a residential setting.

However, if your loved one lives in an assisted living community and qualifies for Medicare home health services, those skilled nursing and therapy visits can be covered by Medicare while they live there. The assisted living facility provides the housing and daily assistance. Medicare covers the medical services delivered in that setting, assuming all eligibility requirements are met.

But the $4,500 to $6,500 per month your family pays for the assisted living community itself? That comes out of your pocket, from long-term care insurance, VA benefits, Medicaid, or other private funds. Medicare will not help with that cost.

Medicare and Hospice Care

Medicare Part A covers hospice care when a doctor certifies that a patient has a terminal illness with a life expectancy of six months or less. Hospice is one of the most comprehensive Medicare benefits available, and many families don’t take advantage of it soon enough.

Under the hospice benefit, Medicare covers:

Doctor services and nursing care. Medical equipment and supplies. Prescription drugs for pain management and symptom control. Aide and homemaker services. Physical therapy, occupational therapy, and speech therapy for comfort and quality of life. Grief and loss counseling for family members. Short-term inpatient care for pain and symptom management. Respite care to give family caregivers a break — up to 5 consecutive days.

The family pays very little — a small copayment for outpatient drugs and a 5% coinsurance for inpatient respite care. Most hospice services are provided in the patient’s home, including assisted living facilities.

Hospice is about comfort and quality of life, not giving up. Many families wait too long to consider hospice because they think it means “stopping treatment.” In reality, it means shifting the focus to keeping your loved one comfortable and surrounded by support. I’ve seen hospice care transform the final months of a patient’s life — and give families peace they never expected.

The Medicare Advantage Problem — What I Saw Running an Agency

Medicare Advantage plans — the private insurance plans under Medicare Part C — deserve their own honest discussion. These plans are heavily marketed to seniors because many have low or zero monthly premiums and include extras like dental, vision, and hearing coverage. On paper, they look like a great deal.

In practice, I watched them create serious problems for families trying to get care.

The prior authorization nightmare. When your loved one needs home health care, physical therapy, or durable medical equipment under a Medicare Advantage plan, the provider usually has to get prior authorization from the insurance company before starting services. Data from 2026 shows that 99% of Advantage plans require prior authorization for home health care. This process can take 3 to 7 business days — or longer. If your parent just came home from the hospital and needs immediate nursing care, waiting a week for authorization is not just inconvenient, it can be medically dangerous.

But the problems go deeper than just delays. Most Advantage plans authorize specific services at specific frequencies. If your loved one’s doctor orders physical therapy three times per week, the insurance may only authorize two. If the doctor orders skilled nursing twice a week for wound care, the plan may approve once. Families often don’t find out about these reductions until after care has started — or worse, until they get a denial letter weeks later.

The provider network illusion. This is what I saw over and over during 13 years running an agency: families would call us desperately looking for home health care, unable to find any provider willing to accept their Medicare Advantage plan. They’d tell me their plan’s website showed dozens of agencies in the network. But when they actually called those agencies, none would take them.

Why does this happen? Some Medicare Advantage plans reimburse providers so poorly that agencies simply cannot afford to accept those patients. If the reimbursement doesn’t cover the cost of sending a qualified nurse to a patient’s home, plus mileage, plus medical supplies — the agency loses money on every single visit. No business can survive that.

In 2026, CMS finalized a 1.3% aggregate decrease in payments to home health providers, which includes a 3% temporary adjustment. This means agencies are being even more selective about which patients and which plans they accept. The financial pressure on providers is real, and the families caught in the middle pay the price.

This problem is especially bad with certain low-cost Medicare Advantage programs. The plans advertise large provider networks to attract enrollment, but the network exists on paper only. When a patient actually needs care, those providers either aren’t accepting new patients under that plan or have quietly stopped participating altogether.

The appeal process. When services are denied or reduced under a Medicare Advantage plan, families have the right to appeal. But the appeal process is time-consuming, confusing, and emotionally draining — especially when you’re already dealing with a loved one’s health crisis. Many families give up and pay out of pocket rather than fight the insurance company.

The Durable Medical Equipment Disappointment

Durable medical equipment — hospital beds, wheelchairs, walkers, oxygen equipment, nebulizers, commodes, and other medical devices — is covered by Medicare Part B when prescribed by a doctor and deemed medically necessary. The patient typically pays 20% of the Medicare-approved amount after meeting the Part B deductible.

But here’s what the brochures don’t tell you: the quality of Medicare-supplied equipment is often very basic. After years of working with families who received DME through Medicare, I can tell you that many were genuinely surprised — and disappointed — by what showed up at their door.

The wheelchair may be functional but uncomfortable for extended use. The hospital bed may be a basic model without features that would make care easier. The walker may be the most basic design available. Families frequently end up purchasing higher-quality replacements from a private DME supplier at their own expense — essentially paying twice.

The authorization process for DME is another source of frustration. Getting approval for equipment requires documentation from the doctor, specific medical justification, and sometimes additional evaluations. The paperwork is extensive, the process is slow, and the items don’t always arrive when you need them. I’ve seen patients wait weeks for equipment that should have been available within days of discharge.

For Medicare Advantage plans, the DME process adds another layer of complexity because the plan may require prior authorization and may limit which DME suppliers you can use.

My advice: if your loved one needs medical equipment urgently, consider renting or purchasing it privately while waiting for Medicare approval. You can always submit for reimbursement later, but don’t let your parent go without a needed walker or hospital bed because of paperwork delays.

Choose Your Medicare Plan Carefully — This Could Save You Thousands

If you or your loved one anticipates needing medical services — especially home health care, therapy, or medical equipment — the choice between Original Medicare with a Medigap supplement versus a Medicare Advantage plan is one of the most important financial decisions you’ll make.

Here’s my advice after 13 years on the provider side:

Original Medicare with a Medigap supplement gives you the most flexibility. You can use any Medicare-certified provider in the country. There are no network restrictions, no prior authorization requirements for most services, and no referrals needed. Medigap plans cover the gaps — the deductibles and coinsurance that Original Medicare leaves behind. The trade-off is higher monthly premiums, but you get freedom of choice and faster access to care.

Medicare Advantage plans have lower monthly premiums — sometimes zero — but come with network restrictions, prior authorization requirements, and the provider availability problems I described above. They can work well for healthy seniors who primarily need preventive care. But when serious medical needs arise, the limitations become painful.

Before choosing any Medicare plan, do this: call two or three home health agencies, medical equipment suppliers, and therapy providers in your area. Ask them directly which Medicare plans they accept and which ones they avoid. Their answers will tell you more about the real-world value of a plan than any marketing brochure or provider directory ever will.

A plan that costs $20 or $30 more per month but gives you access to quality providers who will actually accept your loved one is worth far more than a free plan that leaves you desperately searching for care when you need it most.

What About Texas Medicaid?

For families who cannot afford to pay for care privately, Texas Medicaid may help — but it’s a separate program from Medicare with its own eligibility rules.

Texas Medicaid covers long-term care services through the STAR+PLUS waiver program, which provides home and community-based services including personal attendant care, home modifications, and assisted living services. To qualify, a single person’s income generally cannot exceed approximately $2,982 per month, and assets are limited to about $2,000.

If your loved one has both Medicare and Medicaid (known as being “dual eligible”), they may receive benefits from both programs. Medicare covers the medical services, while Medicaid covers the long-term care and support services that Medicare does not.

However, there is a significant waitlist for STAR+PLUS waiver services. As of late 2025, roughly 15,000 to 16,000 people were on the Texas STAR+PLUS interest list. This is not a quick solution — families should plan for months or even years of waiting.

For more information about Texas Medicaid eligibility and the application process, contact the Texas Health and Human Services Commission.

How to Protect Your Family Financially

Based on everything I’ve seen working with hundreds of families, here is the financial planning advice I would give to anyone caring for an aging loved one:

Do not build your care plan around Medicare coverage. Treat Medicare as a helpful supplement for specific medical services — not as the foundation of your long-term care funding. Budget based on what you’ll likely pay privately.

Understand the real costs before you need care. Research the cost of home caregivers, assisted living, and skilled nursing facilities in your area now — not during a crisis. Knowing the numbers helps you make calm, informed decisions.

If you haven’t enrolled in Medicare yet, choose your plan carefully. Talk to providers in your area before selecting a plan. The cheapest option upfront may cost you far more in the long run through limited access to care.

If your loved one has a Medicare Advantage plan and is having trouble finding providers, consider switching to Original Medicare during the annual enrollment period. This is October 15 through December 7 each year. You may also qualify for a Medigap plan, though availability and pricing may depend on when you apply.

Look into all funding sources. Long-term care insurance, VA Aid and Attendance benefits, life insurance conversion, Texas Medicaid, and family resources should all be explored. Many families qualify for benefits they don’t know about.

Keep records of everything. Every doctor’s order, every authorization, every denial letter. If you need to appeal a Medicare decision, documentation is your strongest weapon.

Don’t wait until a crisis. The worst time to make care decisions is in the hospital at 11pm when a discharge planner tells you your parent can’t go home alone. Start planning now, while you can think clearly and explore options without pressure.

Common Medicare Questions Families Ask

“Does Medicare cover assisted living?”

No. Medicare does not cover the cost of assisted living. It may cover medical services like home health visits or therapy that your loved one receives while living in an assisted living community, but not the room, board, or monthly rent.

“Does Medicare cover 24-hour home care?”

No. Medicare covers part-time, intermittent skilled care — not 24-hour caregivers or live-in aides. For around-the-clock home care, families typically pay privately, use long-term care insurance, or explore Medicaid waiver programs.

“How long does Medicare cover home health?”

There is no fixed time limit. Coverage continues as long as your loved one meets all eligibility requirements and the doctor recertifies the need every 60 days. However, coverage ends when the skilled need is met or the patient is no longer homebound.

“My parent’s Medicare Advantage plan denied home health care. What can we do?”

You have the right to appeal. Contact the plan directly and request a written explanation of the denial. Then file an appeal with supporting documentation from your loved one’s doctor. If the first appeal is denied, you can request an independent review. Consider contacting the Medicare rights helpline at 1-800-MEDICARE (1-800-633-4227) for guidance.

“Does Medicare pay for a caregiver if I’m a family member?”

No. Medicare does not pay family members to provide care. However, Texas Medicaid’s Consumer Directed Services option under STAR+PLUS may allow a family member to be paid as an attendant in some situations.

“Is Original Medicare better than Medicare Advantage?”

It depends on your health needs and financial situation. For seniors who are mostly healthy and primarily need preventive care, Medicare Advantage can be a good value. For seniors with complex medical needs who anticipate needing home health, therapy, or medical equipment, Original Medicare with a Medigap supplement often provides better access to providers and fewer authorization hurdles. Talk to providers in your area to understand which plans they accept before deciding.

“What if Medicare denies coverage and I can’t afford to pay?”

Contact your local Area Agency on Aging, which can connect you with resources and programs that may help. Also explore Texas Medicaid eligibility, VA benefits if your loved one is a veteran or veteran’s spouse, and nonprofit organizations that provide financial assistance for senior care.

Need Help Navigating Medicare and Senior Care?

Medicare is complicated, and the stakes are too high for guesswork. At RightCareFinder, we help Texas families understand their options and find the right care — whether that’s home health, assisted living, memory care, skilled nursing, or hospice. Every case is personally reviewed by a registered nurse who has spent over a decade working within this system.

We know what Medicare covers because we’ve billed it. We know what Medicare Advantage plans actually accept because we’ve called every one of them. And we know what families go through because we’ve walked beside them through it.

Our service is completely free for families. Get nurse-guided help at RightCareFinder.com or click Get Free Help Now.

This article is for informational purposes only and does not constitute medical, financial, or legal advice. Medicare rules, premiums, and coverage can change annually. Always verify current information directly with Medicare at 1-800-MEDICARE (1-800-633-4227) or at medicare.gov. Information about 2026 costs and coverage is based on CMS announcements and publicly available data.Understanding Medicare coverage for senior care can mean the difference between financial security and financial disaster for your family.

After 13 years of running a home health agency in Texas and over 30 years as a registered nurse, I can tell you the single biggest financial mistake families make when planning for a loved one’s care: they assume Medicare will cover most of it.

It won’t. And by the time families realize this, they’ve already made decisions based on a plan that doesn’t exist.

This guide is the article I wish every family would read before they need care. I’m going to walk you through what Medicare actually covers, what it doesn’t, the hidden pitfalls of Medicare Advantage plans, the disappointing reality of Medicare equipment, and the one piece of advice that could save your family thousands of dollars. This comes from someone who dealt with Medicare every single day for over a decade — not from someone who read a government brochure.

Understanding the Basics — Medicare Part A vs Part B

Before we get into specifics, you need to understand how Medicare is structured. Medicare has multiple parts, and each one covers different things.

Medicare Part A is sometimes called hospital insurance. It covers inpatient hospital stays, skilled nursing facility care after a qualifying hospital stay, hospice care, and some home health services. Most people don’t pay a monthly premium for Part A because they or their spouse paid Medicare taxes while working for at least 10 years.

Medicare Part B is sometimes called medical insurance. It covers doctor visits, outpatient care, certain home health services, durable medical equipment, and preventive services. In 2026, the standard Part B premium is approximately $185 per month, and the annual deductible is $257.

Medicare Part C is Medicare Advantage — these are private insurance plans that bundle Part A and Part B together, often with additional benefits. We’ll talk about the significant pros and cons of these plans below.

Medicare Part D covers prescription drugs. It’s a separate plan you enroll in, and the costs vary widely depending on which plan you choose.

Understanding which part covers what is critical because families constantly mix them up — and that confusion leads to nasty financial surprises.

What Medicare Covers for Home Health Care

Medicare covers home health care — but only under very specific conditions. This is where most of the confusion and frustration begins.

To qualify for Medicare home health services, your loved one must meet all four of these requirements at the same time:

First, a doctor must order the care. A physician, nurse practitioner, or physician assistant must certify that your loved one needs home health services and create a written plan of care. Without this doctor’s order, Medicare will not pay for anything — period.

Second, your loved one must be homebound. This does not mean they can never leave the house. It means leaving home requires a considerable and taxing effort. They can still go to medical appointments, attend church, go to adult day care, or get a haircut. But if they need help from another person or a device like a walker or wheelchair to leave the house, or if their condition makes leaving inadvisable, they generally qualify as homebound.

Third, they must need skilled care. This means they require skilled nursing (wound care, IV therapy, medication management, catheter care, injections, disease education) or skilled therapy (physical therapy, occupational therapy, or speech therapy). Simply needing help with bathing, dressing, or meals is not enough on its own — there must be a skilled need.

Fourth, the care must be part-time or intermittent. Medicare typically covers up to 8 hours per day of combined skilled nursing and aide services, with a maximum of 28 hours per week. In some situations, this can be extended to 35 hours per week for a short period. Medicare does not cover 24-hour care, live-in caregivers, or long-term continuous care at home.

If your loved one meets all four criteria, Medicare covers these services at no cost to the family — no copay, no deductible for home health services:

Skilled nursing visits for wound care, medication management, IV therapy, injections, catheter care, patient and caregiver education, and disease management.

Physical therapy to improve strength, mobility, and balance — or to maintain current function and prevent decline.

Occupational therapy to help with daily activities and improve independence.

Speech-language pathology for speech, language, and swallowing difficulties.

Medical social work services to help with emotional, social, and financial concerns related to the illness.

Home health aide services for personal care like bathing, dressing, and grooming — but only if skilled nursing or therapy services are also being provided. The aide cannot be the only service.

Certain medical supplies related to the plan of care, like wound dressings and catheters.

What Medicare Does NOT Cover at Home

This is the list that catches families off guard:

24-hour home care or live-in caregivers. Medicare is not a long-term care program. It is designed for short-term, skilled, intermittent care to help someone recover or stabilize — not for ongoing custodial support.

Homemaker services on their own. Cooking, cleaning, laundry, and grocery shopping are not covered unless a home health aide provides them as part of a broader plan that includes skilled services.

Personal care alone. If your loved one only needs help with bathing and dressing but has no skilled nursing or therapy need, Medicare will not pay. This is the most common reason families are denied coverage, and it’s the one that causes the most frustration.

Meal delivery services. Programs like Meals on Wheels are wonderful, but they are not covered by Medicare.

Companionship. If your parent is lonely and needs someone to sit with them or take them for walks, that is not a Medicare-covered service.

Prescription medications at home. Part D covers prescriptions separately — home health coverage under Part A and B does not include drug coverage.

How Long Does Medicare Home Health Last?

There is no fixed day limit for Medicare home health. Coverage continues as long as your loved one continues to meet all four eligibility criteria and the doctor recertifies the need every 60 days.

I’ve had patients receive Medicare home health services for months — sometimes over a year — as long as there was a documented skilled need and they remained homebound. However, Medicare will stop coverage when the skilled need has been fully met, the patient is no longer homebound, or the doctor discontinues the order.

An important protection families should know about: the Jimmo settlement established that Medicare cannot deny home health coverage simply because a patient is not improving. If skilled care is needed to maintain current function or slow a decline, that is a valid reason for continued coverage. You do not have to show progress to keep your benefits.

What Medicare Covers in a Skilled Nursing Facility

If your loved one needs care in a skilled nursing facility after a hospital stay, Medicare Part A may cover it — but the rules are strict and the coverage is limited.

To qualify, your loved one must have had a qualifying inpatient hospital stay of at least 3 consecutive days. Time spent in the emergency room or under observation status does not count toward those 3 days — and this is a trap that catches many families. If the hospital classified your loved one as “observation” rather than “inpatient,” they may not qualify for SNF coverage even after being in the hospital for several days.

If they qualify, here’s what Medicare covers:

Days 1 through 20: Medicare pays 100% of covered services. No cost to the family.

Days 21 through 100: The family pays a daily coinsurance of $217 per day in 2026. Medicare covers the rest. If you have a Medigap supplemental policy, it may cover this coinsurance.

Days 101 and beyond: Medicare pays nothing. The family is responsible for 100% of the cost. At current Texas rates, that can be $7,000 to $7,500 per month for a private room.

Coverage also ends if your loved one’s care shifts from “skilled” to “custodial” — meaning they no longer need active medical treatment or therapy and are simply receiving help with daily activities. This transition can happen quickly, and families are often surprised when coverage stops well before day 100.

Medicare and Assisted Living — The Hard Truth

Here’s the blunt truth: Medicare does not pay for assisted living. Not the room, not the board, not the monthly rent. Assisted living is not considered a medical facility under Medicare — it’s a residential setting.

However, if your loved one lives in an assisted living community and qualifies for Medicare home health services, those skilled nursing and therapy visits can be covered by Medicare while they live there. The assisted living facility provides the housing and daily assistance. Medicare covers the medical services delivered in that setting, assuming all eligibility requirements are met.

But the $4,500 to $6,500 per month your family pays for the assisted living community itself? That comes out of your pocket, from long-term care insurance, VA benefits, Medicaid, or other private funds. Medicare will not help with that cost.

Medicare and Hospice Care

Medicare Part A covers hospice care when a doctor certifies that a patient has a terminal illness with a life expectancy of six months or less. Hospice is one of the most comprehensive Medicare benefits available, and many families don’t take advantage of it soon enough.

Under the hospice benefit, Medicare covers:

Doctor services and nursing care. Medical equipment and supplies. Prescription drugs for pain management and symptom control. Aide and homemaker services. Physical therapy, occupational therapy, and speech therapy for comfort and quality of life. Grief and loss counseling for family members. Short-term inpatient care for pain and symptom management. Respite care to give family caregivers a break — up to 5 consecutive days.

The family pays very little — a small copayment for outpatient drugs and a 5% coinsurance for inpatient respite care. Most hospice services are provided in the patient’s home, including assisted living facilities.

Hospice is about comfort and quality of life, not giving up. Many families wait too long to consider hospice because they think it means “stopping treatment.” In reality, it means shifting the focus to keeping your loved one comfortable and surrounded by support. I’ve seen hospice care transform the final months of a patient’s life — and give families peace they never expected.

The Medicare Advantage Problem — What I Saw Running an Agency

Medicare Advantage plans — the private insurance plans under Medicare Part C — deserve their own honest discussion. These plans are heavily marketed to seniors because many have low or zero monthly premiums and include extras like dental, vision, and hearing coverage. On paper, they look like a great deal.

In practice, I watched them create serious problems for families trying to get care.

The prior authorization nightmare. When your loved one needs home health care, physical therapy, or durable medical equipment under a Medicare Advantage plan, the provider usually has to get prior authorization from the insurance company before starting services. Data from 2026 shows that 99% of Advantage plans require prior authorization for home health care. This process can take 3 to 7 business days — or longer. If your parent just came home from the hospital and needs immediate nursing care, waiting a week for authorization is not just inconvenient, it can be medically dangerous.

But the problems go deeper than just delays. Most Advantage plans authorize specific services at specific frequencies. If your loved one’s doctor orders physical therapy three times per week, the insurance may only authorize two. If the doctor orders skilled nursing twice a week for wound care, the plan may approve once. Families often don’t find out about these reductions until after care has started — or worse, until they get a denial letter weeks later.

The provider network illusion. This is what I saw over and over during 13 years running an agency: families would call us desperately looking for home health care, unable to find any provider willing to accept their Medicare Advantage plan. They’d tell me their plan’s website showed dozens of agencies in the network. But when they actually called those agencies, none would take them.

Why does this happen? Some Medicare Advantage plans reimburse providers so poorly that agencies simply cannot afford to accept those patients. If the reimbursement doesn’t cover the cost of sending a qualified nurse to a patient’s home, plus mileage, plus medical supplies — the agency loses money on every single visit. No business can survive that.

In 2026, CMS finalized a 1.3% aggregate decrease in payments to home health providers, which includes a 3% temporary adjustment. This means agencies are being even more selective about which patients and which plans they accept. The financial pressure on providers is real, and the families caught in the middle pay the price.

This problem is especially bad with certain low-cost Medicare Advantage programs. The plans advertise large provider networks to attract enrollment, but the network exists on paper only. When a patient actually needs care, those providers either aren’t accepting new patients under that plan or have quietly stopped participating altogether.

The appeal process. When services are denied or reduced under a Medicare Advantage plan, families have the right to appeal. But the appeal process is time-consuming, confusing, and emotionally draining — especially when you’re already dealing with a loved one’s health crisis. Many families give up and pay out of pocket rather than fight the insurance company.

The Durable Medical Equipment Disappointment

Durable medical equipment — hospital beds, wheelchairs, walkers, oxygen equipment, nebulizers, commodes, and other medical devices — is covered by Medicare Part B when prescribed by a doctor and deemed medically necessary. The patient typically pays 20% of the Medicare-approved amount after meeting the Part B deductible.

But here’s what the brochures don’t tell you: the quality of Medicare-supplied equipment is often very basic. After years of working with families who received DME through Medicare, I can tell you that many were genuinely surprised — and disappointed — by what showed up at their door.

The wheelchair may be functional but uncomfortable for extended use. The hospital bed may be a basic model without features that would make care easier. The walker may be the most basic design available. Families frequently end up purchasing higher-quality replacements from a private DME supplier at their own expense — essentially paying twice.

The authorization process for DME is another source of frustration. Getting approval for equipment requires documentation from the doctor, specific medical justification, and sometimes additional evaluations. The paperwork is extensive, the process is slow, and the items don’t always arrive when you need them. I’ve seen patients wait weeks for equipment that should have been available within days of discharge.

For Medicare Advantage plans, the DME process adds another layer of complexity because the plan may require prior authorization and may limit which DME suppliers you can use.

My advice: if your loved one needs medical equipment urgently, consider renting or purchasing it privately while waiting for Medicare approval. You can always submit for reimbursement later, but don’t let your parent go without a needed walker or hospital bed because of paperwork delays.

Choose Your Medicare Plan Carefully — This Could Save You Thousands

If you or your loved one anticipates needing medical services — especially home health care, therapy, or medical equipment — the choice between Original Medicare with a Medigap supplement versus a Medicare Advantage plan is one of the most important financial decisions you’ll make.

Here’s my advice after 13 years on the provider side:

Original Medicare with a Medigap supplement gives you the most flexibility. You can use any Medicare-certified provider in the country. There are no network restrictions, no prior authorization requirements for most services, and no referrals needed. Medigap plans cover the gaps — the deductibles and coinsurance that Original Medicare leaves behind. The trade-off is higher monthly premiums, but you get freedom of choice and faster access to care.

Medicare Advantage plans have lower monthly premiums — sometimes zero — but come with network restrictions, prior authorization requirements, and the provider availability problems I described above. They can work well for healthy seniors who primarily need preventive care. But when serious medical needs arise, the limitations become painful.

Before choosing any Medicare plan, do this: call two or three home health agencies, medical equipment suppliers, and therapy providers in your area. Ask them directly which Medicare plans they accept and which ones they avoid. Their answers will tell you more about the real-world value of a plan than any marketing brochure or provider directory ever will.

A plan that costs $20 or $30 more per month but gives you access to quality providers who will actually accept your loved one is worth far more than a free plan that leaves you desperately searching for care when you need it most.

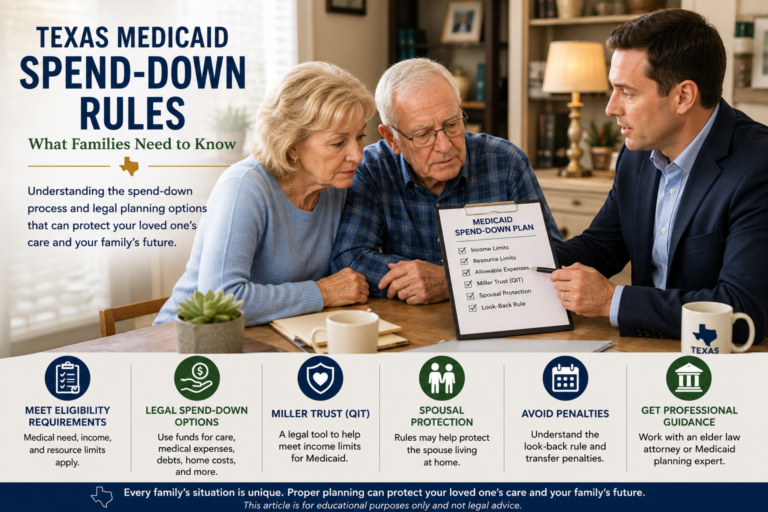

What About Texas Medicaid?

For families who cannot afford to pay for care privately, Texas Medicaid may help — but it’s a separate program from Medicare with its own eligibility rules.

Texas Medicaid covers long-term care services through the STAR+PLUS waiver program, which provides home and community-based services including personal attendant care, home modifications, and assisted living services. To qualify, a single person’s income generally cannot exceed approximately $2,982 per month, and assets are limited to about $2,000.

If your loved one has both Medicare and Medicaid (known as being “dual eligible”), they may receive benefits from both programs. Medicare covers the medical services, while Medicaid covers the long-term care and support services that Medicare does not.

However, there is a significant waitlist for STAR+PLUS waiver services. As of late 2025, roughly 15,000 to 16,000 people were on the Texas STAR+PLUS interest list. This is not a quick solution — families should plan for months or even years of waiting.

For more information about Texas Medicaid eligibility and the application process, contact the Texas Health and Human Services Commission.

How to Protect Your Family Financially

Based on everything I’ve seen working with hundreds of families, here is the financial planning advice I would give to anyone caring for an aging loved one:

Do not build your care plan around Medicare coverage. Treat Medicare as a helpful supplement for specific medical services — not as the foundation of your long-term care funding. Budget based on what you’ll likely pay privately.

Understand the real costs before you need care. Research the cost of home caregivers, assisted living, and skilled nursing facilities in your area now — not during a crisis. Knowing the numbers helps you make calm, informed decisions.

If you haven’t enrolled in Medicare yet, choose your plan carefully. Talk to providers in your area before selecting a plan. The cheapest option upfront may cost you far more in the long run through limited access to care.

If your loved one has a Medicare Advantage plan and is having trouble finding providers, consider switching to Original Medicare during the annual enrollment period. This is October 15 through December 7 each year. You may also qualify for a Medigap plan, though availability and pricing may depend on when you apply.

Look into all funding sources. Long-term care insurance, VA Aid and Attendance benefits, life insurance conversion, Texas Medicaid, and family resources should all be explored. Many families qualify for benefits they don’t know about.

Keep records of everything. Every doctor’s order, every authorization, every denial letter. If you need to appeal a Medicare decision, documentation is your strongest weapon.

Don’t wait until a crisis. The worst time to make care decisions is in the hospital at 11pm when a discharge planner tells you your parent can’t go home alone. Start planning now, while you can think clearly and explore options without pressure.

Common Medicare Questions Families Ask

“Does Medicare cover assisted living?”

No. Medicare does not cover the cost of assisted living. It may cover medical services like home health visits or therapy that your loved one receives while living in an assisted living community, but not the room, board, or monthly rent.

“Does Medicare cover 24-hour home care?”

No. Medicare covers part-time, intermittent skilled care — not 24-hour caregivers or live-in aides. For around-the-clock home care, families typically pay privately, use long-term care insurance, or explore Medicaid waiver programs.

“How long does Medicare cover home health?”

There is no fixed time limit. Coverage continues as long as your loved one meets all eligibility requirements and the doctor recertifies the need every 60 days. However, coverage ends when the skilled need is met or the patient is no longer homebound.

“My parent’s Medicare Advantage plan denied home health care. What can we do?”

You have the right to appeal. Contact the plan directly and request a written explanation of the denial. Then file an appeal with supporting documentation from your loved one’s doctor. If the first appeal is denied, you can request an independent review. Consider contacting the Medicare rights helpline at 1-800-MEDICARE (1-800-633-4227) for guidance.

“Does Medicare pay for a caregiver if I’m a family member?”

No. Medicare does not pay family members to provide care. However, Texas Medicaid’s Consumer Directed Services option under STAR+PLUS may allow a family member to be paid as an attendant in some situations.

“Is Original Medicare better than Medicare Advantage?”

It depends on your health needs and financial situation. For seniors who are mostly healthy and primarily need preventive care, Medicare Advantage can be a good value. For seniors with complex medical needs who anticipate needing home health, therapy, or medical equipment, Original Medicare with a Medigap supplement often provides better access to providers and fewer authorization hurdles. Talk to providers in your area to understand which plans they accept before deciding.

“What if Medicare denies coverage and I can’t afford to pay?”

Contact your local Area Agency on Aging, which can connect you with resources and programs that may help. Also explore Texas Medicaid eligibility, VA benefits if your loved one is a veteran or veteran’s spouse, and nonprofit organizations that provide financial assistance for senior care.

Need Help Navigating Medicare and Senior Care?

Medicare is complicated, and the stakes are too high for guesswork. At RightCareFinder, we help Texas families understand their options and find the right care — whether that’s home health, assisted living, memory care, skilled nursing, or hospice. Every case is personally reviewed by a registered nurse who has spent over a decade working within this system.

We know what Medicare covers because we’ve billed it. We know what Medicare Advantage plans actually accept because we’ve called every one of them. And we know what families go through because we’ve walked beside them through it.

Our service is completely free for families. Get nurse-guided help at RightCareFinder.com or click Get Free Help Now.

This article is for informational purposes only and does not constitute medical, financial, or legal advice. Medicare rules, premiums, and coverage can change annually. Always verify current information directly with Medicare at 1-800-MEDICARE (1-800-633-4227) or at medicare.gov. Information about 2026 costs and coverage is based on CMS announcements and publicly available data.