Texas Medicaid Spend-Down Rules: What Every Family Must Know (2026)

When a parent or spouse suddenly needs nursing home care, memory care, or long-term support, many Texas families discover a painful truth: senior care is devastatingly expensive, and Medicare does not pay for long-term custodial care. That’s when someone says “You need to spend down for Medicaid,” and the panic begins. Understanding the Medicaid spend-down rules in Texas can mean the difference between protecting your family’s finances and making mistakes that cost you everything.

As a registered nurse with over 30 years of experience, a PhD in Clinical Psychology, and over 13 years working with families navigating these exact situations, I have watched families drain their life savings because they didn’t understand the rules and I’ve watched other families protect themselves because they got the right guidance early. This article gives you the honest truth about how Medicaid spend-down works in Texas, what legal tools can help, and the mistakes that can devastate your family financially.

Important: This article is for education only. Medicaid rules are complex and can change. Families should speak with a qualified elder-law attorney, Medicaid planner, or Texas benefits professional before making any financial transfers or legal decisions.

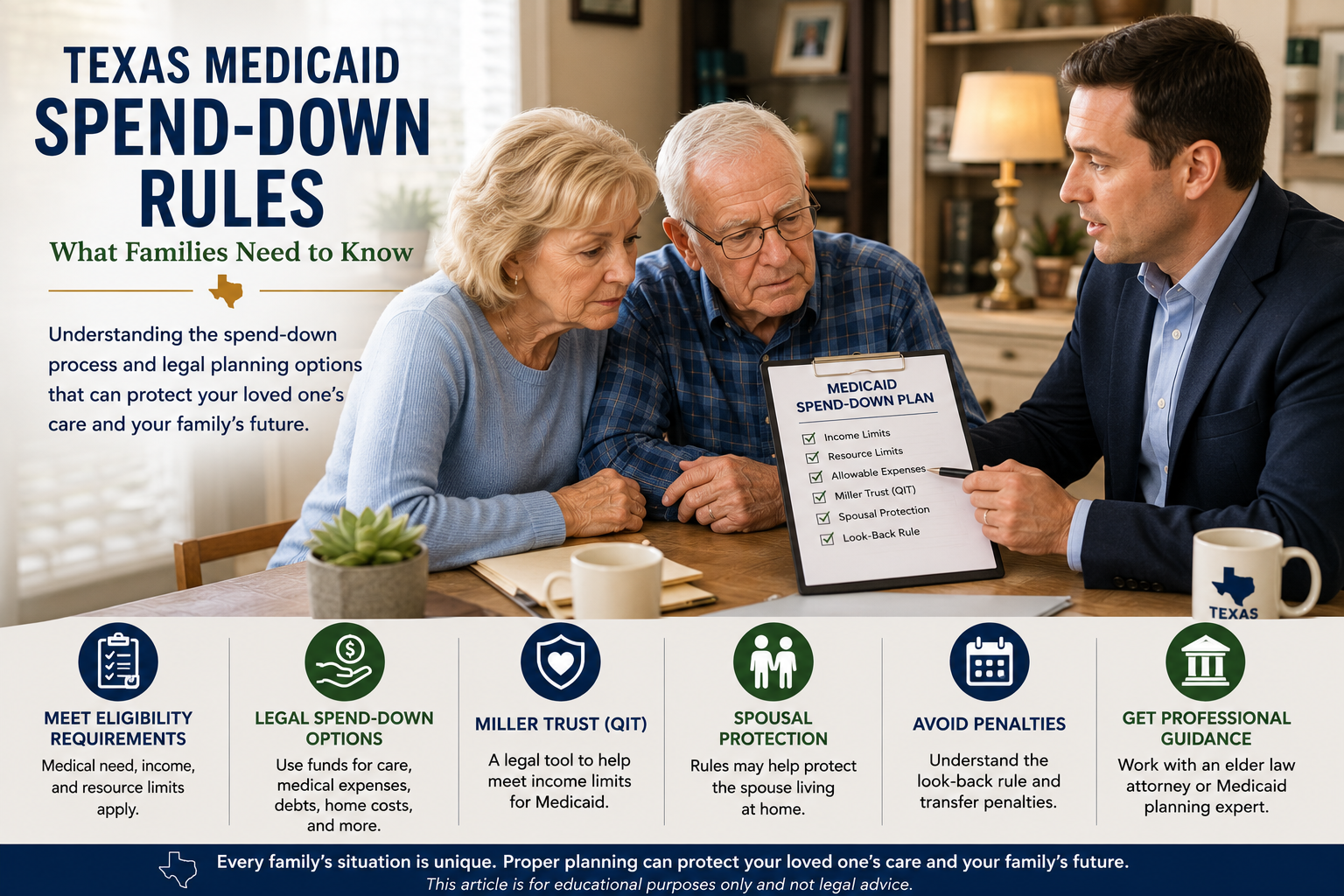

What Does Medicaid Spend-Down Actually Mean?

In simple terms, a Medicaid spend-down means using a person’s own money or assets in legally allowable ways so they can meet Medicaid’s strict financial eligibility requirements for long-term care.

For Texas long-term care Medicaid whether nursing home Medicaid or the STAR+PLUS Home and Community-Based Services waiver eligibility depends on three things: medical need (the person requires a nursing home level of care), income rules (monthly income must be below a specific cap), and resource or asset rules (countable assets must be below a strict limit).

Spend-down is not about hiding money. It is not about giving money away to your children. It is about using funds legally for the senior’s care, medical needs, debts, home safety, and other allowable purposes with proper documentation every step of the way.

The 2026 Texas Medicaid Financial Limits

Texas is one of the strictest states in the country when it comes to long-term care Medicaid eligibility. Here are the numbers families need to know:

Asset limit for a single applicant: $2,000 in countable resources. That is not a typo. Two thousand dollars is all a single person can have in countable assets to qualify.

Countable assets include checking and savings accounts, stocks, bonds, mutual funds, cryptocurrency, CDs, and real estate that is not the primary home.

Exempt assets — things that do NOT count against the limit — include the primary residence (up to a $752,000 equity limit if single, or completely exempt if a spouse lives there), one vehicle of any value, household furnishings and personal effects, and irrevocable burial funds that have been properly set up.

Important exception for retirement accounts: In Texas, IRAs and 401(k)s may be considered exempt if they are in “payout status” meaning the owner is actively taking their Required Minimum Distribution. This is a detail that many families and even some advisors miss.

Income limit for a single applicant: $2,982 per month gross income. If your loved one’s monthly income exceeds this amount by even one dollar, they are technically disqualified — unless they use a legal tool called a Qualified Income Trust.

The Miller Trust — The Tool That Solves the Income Problem

One of the most important legal tools Texas families need to understand is the Qualified Income Trust, commonly called a Miller Trust.

Texas is an income-cap state. If an applicant’s gross monthly income is above the $2,982 limit, they cannot qualify for long-term care Medicaid through regular channels no matter how sick they are or how little money they have in the bank. This is where the Miller Trust comes in.

A Miller Trust is a special bank account set up according to specific legal requirements. Each month, the applicant’s income that exceeds the Medicaid limit is deposited into this trust account. The trust then distributes the funds according to Medicaid rules paying for the patient’s personal needs allowance, the spouse’s maintenance needs, and the remainder to the nursing facility.

This is not a way to hide income. It is a legal structure recognized by Texas Medicaid that routes income according to program requirements. The trust must be set up correctly, funded properly every single month, and administered according to the rules. Families should not attempt to create one without an elder-law attorney.

A Miller Trust may be needed when the senior’s monthly income from Social Security, pension, retirement, and other sources exceeds $2,982, they medically need nursing home care or STAR+PLUS waiver services, and they would otherwise qualify for Medicaid except for the income cap.

The 5-Year Look-Back Rule. The Trap That Catches Families

This is where families get into the most serious trouble. Texas Medicaid reviews the applicant’s financial records for the 60 months — five full years — prior to the Medicaid application date. Every bank statement, every transfer, every large purchase is examined.

If a person gave away assets, transferred money to family members, or sold property for less than fair market value during this look-back period, Medicaid imposes a penalty period. During the penalty period, Medicaid refuses to pay for care but the nursing home still needs to be paid. The family is stuck covering the full cost out of pocket.

The penalty period is calculated by dividing the total value of improper transfers by the average monthly cost of private-pay nursing facility care in the region. A $40,000 gift could create a penalty of several months where Medicaid won’t pay a cent.

A real example: A Texas family knew their father was developing severe Alzheimer’s disease. Wanting to help his grandson buy a house, the father gifted him $40,000. Two years later, the father’s condition declined rapidly, his private funds were exhausted, and he needed a secure nursing facility. When the family applied for Medicaid, the caseworker flagged the $40,000 gift during the five-year look-back review. Medicaid imposed a penalty period of several months, refusing to pay for nursing home care during that time. The family was forced to scramble to find cash to pay the facility privately during the penalty window. They deeply regretted the unguided gift.

This is why families should never “just put the house in the children’s names” or “empty the bank account” or “give everyone their inheritance early” without professional legal advice. What feels like smart planning can become a financial disaster.

Community Spouse Protections.

Preventing Financial Devastation

When one spouse needs nursing home care and the other spouse remains at home, federal and Texas law provide protections to prevent the healthy spouse — called the “community spouse” — from becoming destitute.

This is critically important for married couples. Many families assume that ALL their money must be spent before Medicaid will help. That is not true.

Community Spouse Resource Allowance: When Medicaid evaluates a married couple’s eligibility, all assets are pooled together regardless of whose name is on the account. However, the community spouse is allowed to keep a protected portion. Under the 2026 rules, the community spouse can keep half of the couple’s total countable assets, up to a maximum of $162,660. If half of the assets fall below the state minimum floor of $32,532, the community spouse gets to keep everything up to that floor amount. Only the assets above the approved allowance must be spent down to reach the applicant’s $2,000 limit.

Monthly Maintenance Needs Allowance: If the community spouse has low individual income — for example, a small Social Security check — Texas allows income to be transferred from the institutionalized spouse to the community spouse. The maximum amount that can be transferred in 2026 is $4,066.50 per month. This ensures the spouse at home can afford basic living expenses.

From a clinical psychology perspective, these protections matter enormously. The spouse at home is often already under tremendous emotional stress — grieving, exhausted, frightened about the future. Knowing that they won’t lose everything provides psychological relief that allows them to make calmer, better decisions about their loved one’s care.

What You Can Legally Spend Money On During a Spend-Down

A proper spend-down is not about wasting money or hiding it. It is about using funds for legitimate purposes that benefit the senior. Allowable spending generally includes:

Medical bills, hospital bills, and prescription costs. Dental work, eyeglasses, and hearing aids. Mobility equipment like wheelchairs, walkers, lift chairs, and hospital beds. Home safety modifications such as grab bars, ramps, shower modifications, and improved lighting. Personal care items and clothing. Paying off existing debts like credit cards, car loans, or a mortgage. Prepaid funeral and burial arrangements when set up properly as irrevocable plans. Home repairs that support safety and habitability. Care services including home care and assisted living while funds last.

The critical rule: document everything. Keep every receipt, every invoice, every bank statement, every contract. If you cannot prove where the money went, Medicaid may treat unexplained spending as an improper transfer — and penalize you.

What Families Should Never Do Without Legal Advice

These actions can create serious Medicaid eligibility problems:

Giving large cash gifts to children or grandchildren — this triggers look-back penalties.

Transferring the home to family members without proper legal structure — this can be treated as a gift.

Selling property for less than fair market value — the difference is treated as a gift.

Adding a child’s name to bank accounts — Medicaid may view this as a transfer of half the account balance.

Paying family caregivers informally without a written agreement — without a formal, legally binding caregiver contract at fair market value drafted before the care took place, Medicaid caseworkers will categorize these payments as illegal gifts.

Hiding money or moving funds after a crisis without documentation — this raises red flags during the look-back review.

Assuming “everyone does it” means it is safe — Medicaid caseworkers have seen every trick, and penalties are real.

Legal Strategies to Discuss With an Elder-Law Attorney

When facing a Medicaid spend-down situation, do not act without professional guidance. Elder-law attorneys use legally recognized strategies to help families protect assets while following the rules:

Lady Bird Deed (Enhanced Life Estate Deed): This allows your loved one to keep ownership of their home during their lifetime, but transfers it automatically to their heirs upon death — completely bypassing probate. This matters because Texas has the Medicaid Estate Recovery Program, which can file a claim against the deceased person’s estate to recover what Medicaid spent on their care. Because MERP can only claim against assets that go through probate in Texas, a Lady Bird Deed protects the home from state recovery.

Medicaid-Compliant Annuities: For couples with assets above the Community Spouse Resource Allowance, an attorney may convert excess cash into an irrevocable annuity that pays the community spouse a monthly income stream. This transforms a disqualifying asset into an exempt income source.

Strategic Spend-Down Purchasing: Instead of spending money randomly, an attorney guides the family to spend excess assets on legitimate exempt categories — paying off the mortgage, repairing the family home, upgrading the community spouse’s vehicle, or purchasing irrevocable prepaid funeral contracts.

Qualified Income Trust (Miller Trust): As described above, this legal tool solves the income-cap problem for applicants whose monthly income exceeds the Medicaid limit.

Caregiver Agreements: A properly drafted, legally binding contract that pays a family member fair market value for caregiving services provided before Medicaid application. This must be set up correctly and in advance to avoid being treated as a gift.

How STAR+PLUS Interacts with Spend-Down

STAR+PLUS is the Texas managed care program that delivers Medicaid long-term services and supports, including home and community-based services that can help pay for assisted living, home care, and other support.

If your loved one is trying to access the STAR+PLUS HCBS Waiver, they must pass the exact same financial requirements as someone entering a nursing home — the $2,000 asset limit and the $2,982 income cap.

The critical warning: STAR+PLUS waiver slots are capped, and there is often a long interest list — sometimes months or even years long. As of late 2025, roughly 15,000 to 16,000 people were on the Texas STAR+PLUS interest list. Families who spend down all their money expecting immediate STAR+PLUS approval can find themselves broke and stuck on a waiting list without any care in place. This is one of the most devastating scenarios I’ve seen families face.

Plan for the wait. Do not assume STAR+PLUS will be available quickly.

When Private Pay Runs Out. The Facility Transition

One of the biggest shocks for families is discovering that most private memory care assisted living facilities do not accept Medicaid.

When a resident runs out of private funds in an assisted living memory care community, the facility will typically issue a discharge notice because they do not have a Medicaid contract. The family must then find a skilled nursing facility — a traditional nursing home — that has an available Medicaid bed and offers memory care services.

Once a nursing home accepts the resident as “Medicaid pending,” the state processes the paperwork. After approval, the resident’s monthly income — minus a tiny $75 personal needs allowance — must be paid directly to the nursing home as their required contribution, and Medicaid covers the remaining cost.

This transition is stressful, disorienting, and often traumatic for the resident, especially someone with dementia. Families can reduce the shock by planning for this possibility before funds run out — not after.

Always ask assisted living and memory care communities upfront: “Do you accept Medicaid? If not, what happens when our funds run out? How much private-pay time is required before a Medicaid transition is allowed?”

The Emotional Reality of Spend-Down

Families often feel guilt, shame, fear, and anger around Medicaid planning. Adult children may feel they are “taking Mom’s money.” A spouse may feel ashamed to apply for government assistance after a lifetime of independence. Some families feel rage that a lifetime of hard work and saving is being consumed by care costs.

These emotions are normal and valid.

From a clinical psychology perspective, money becomes symbolic during a health crisis. It represents independence, dignity, security, promises made to a spouse, a legacy for children, and a lifetime of work. When illness threatens all of that, the emotional weight can be crushing.

But Medicaid planning is not about taking advantage of a system. It is about understanding what care your loved one needs, what resources are legally available, and how to follow the rules while protecting safety, dignity, and the family’s financial future.

What Texas Families Should Do Before Spending Down

Before moving any money or making major financial decisions, follow these steps:

Step 1: Gather financial records. Bank statements for the past five years, income records, insurance policies, property records, retirement account statements, and care expense invoices.

Step 2: Gather medical records. Diagnoses, hospital records, medication lists, therapy notes, wound care documentation, and physician recommendations documenting the level of care needed.

Step 3: Document care needs in specific terms. Write down exactly what help is needed with bathing, dressing, toileting, eating, transferring, walking, medications, memory supervision, and safety. Use specific functional language, not vague statements.

Step 4: Contact an elder-law attorney. This is the most important step. Before transferring property, paying family members, creating trusts, or applying for Medicaid after large financial changes, get professional legal guidance. The cost of an attorney is far less than the cost of a Medicaid penalty.

Step 5: Ask about Medicaid eligibility. Contact Texas Health and Human Services or a qualified benefits professional to understand where your loved one stands.

Step 6: Keep every receipt and document every dollar spent. If Medicaid asks where the money went, you need proof.

Quick Reference — Texas Medicaid Spend-Down at a Glance

Single applicant asset limit: $2,000 in countable resources.

Single applicant income limit: $2,982 per month gross income.

Primary home exemption: Up to $752,000 equity (exempt if spouse lives there).

One vehicle: Exempt regardless of value.

Community Spouse Resource Allowance: Up to $162,660 (or minimum floor of $32,532).

Community Spouse Monthly Maintenance: Up to $4,066.50 per month.

Look-back period: 60 months (5 years) of financial records reviewed.

Miller Trust: Required when income exceeds $2,982 per month.

Personal needs allowance in nursing home: $75 per month.

STAR+PLUS interest list: Approximately 15,000 to 16,000 people waiting.

Need Help Navigating Medicaid and Senior Care in Texas?

Understanding Medicaid spend-down rules in Texas is complicated, but you don’t have to figure it out alone. At RightCareFinder, a registered nurse personally reviews your family’s situation and helps you find the right care — whether that means navigating a nursing home transition, finding a Medicaid-accepting facility, or understanding your options before funds run out.

Our service is completely free for families. Get nurse-guided help at RightCareFinder.com or click Get Free Help Now.

This article is for informational purposes only and does not constitute legal, financial, or medical advice. Medicaid rules, income limits, and asset thresholds can change annually. Always verify current information with Texas Health and Human Services or consult with a qualified elder-law attorney before making financial or legal decisions.